$11.5m Sightline Health Settlement: What Can We Learn?

Will Hamilton and Darcy Devine • September 17, 2018

mailto:whamilton@buckheadfmw.comEarlier this year, radiation therapy provider SightLine Health reached a $11.5m settlement with the DOJ in a lawsuit alleging it knowingly violated the federal physician self-referral and anti-kickback laws.

Financial Arrangement

According to the complaint, SightLine’s operating model was to build a radiation therapy center in a new market, and “syndicate” ownership of the center among referring physicians (primarily urologists). Sightline would keep 20% ownership of the JV entity and receive a management fee of $30,000 per month. The referring physicians would individually purchase the remaining 80%, split among 8 to 10 physician-investors who each invested approximately $100,000. The centers were leased to radiation therapists who billed and collected on a global basis and made rent payments to the JV entity for use of the space that allegedly varied based on the volume and value of referrals.

Allegations

The complaint alleges that 1) Sightline violated the Anti-Kickback Statute (“AKS”) by offering physicians the ability to profit, virtually risk-free, in a way that takes into account the volume and value of their referrals to the clinic; 2) the physician-investors violated the AKS by accepting remuneration from Sightline to refer patients; and 3) the physician-investors violated the Stark Law by referring designated health services to centers in which they have an ownership interest.

Potential FMV Issues

Although FMV issues aren’t specifically addressed in the complaint; there may be reason to assume that the plaintiff felt the physician's investments were not made at an FMV price.

Doing some back-of-the-envelope math, the physicians received an 80% interest in a JV entity for a total investment of between $800,000 and $1m, implying a total equity value of $1m to $1.25m. This, of course, is well shy of the cost to build a radiation therapy center with IMRT capabilities – a linear accelerator costs $2.5m to $3m itself, not including buildout. What we don’t know is if financing was used to acquire the facility and equipment – if it was, $1m to $1.25m of equity could theoretically be consistent with FMV.

Another potential FMV issue with the arrangement is that the complaint alleges the physician-investors were offered financing for the $100,000 investment at a 4.5% interest rate, with only the future profits of the venture pledged as collateral. According to the complaint, the investment was typically repaid with center profits within the first year. As a result, the complaint argues that the physicians took on very little financial risk, if any, while receiving significant remuneration.

What Can We Learn?

Since the case settled prior to trial, a lot of key information is unavailable. However, the complaint does include some specifics about the operating model and financial arrangement that provide clues that there may have been FMV-related issues that led to the significant settlement payment, including the investment amounts paid by the physician-investors and the related financing arrangements.

Review the complaint yourself here.

Have a joint venture you'd like reviewed from an FMV perspective? Contact us

We ranked the 30 largest healthcare services and information technology deals of 2018, according to our database, by valuation multiple. The lowest reported price to EBITDA multiples (10x or lower, sorted alphabetically) are listed below.

We ranked the 30 largest healthcare services and information technology deals of 2018, according to our database, by valuation multiple.

We ranked the 30 largest healthcare services and information technology deals of 2018, according to our database, by valuation multiple. The highest reported price to EBITDA multiples (15x or higher, sorted alphabetically) were as follows:

Healthcare services organizations rely on a variety of intangible assets to create business value, including patient and customer relationships, medical records, trade names, assembled workforce, licenses and certifications, non-compete clauses, proprietary technology, software, and others.

For those of you who’ve been involved in a transaction where the only asset transferred is a certificate of need, you’ve probably found that market data is scarce for CON-only deals.

CON Laws, Scope of Practice Restrictions, and Provider Non-Compete Clauses Targeted in New Trump Adm

On Monday, December 3, 2018, the Department of Health and Human Services (HHS) – in collaboration with the Departments of the Treasury and Labor, the Federal Trade Commission, and several offices within the White House – released a report detailing recommendations for improving choice and competition in the healthcare industry.

One of the questions we get asked a lot is how valuations have changed over time.

One of the many benefits of tracking healthcare transactions closely and maintaining a very large database of deals where we can get reliable price to EBITDA and revenue multiples is that it provides insight into profit margins for segments where other financial benchmarking information is sparse.

The most important component of a valuation of an accountable care organization (or other multi-provider network that relies on risk-based shared savings models) is the revenue forecast, which involves “probability-adjusting” future shared savings payments in some manner.

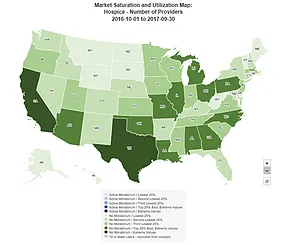

CMS' offers a helpful online tool that shows provider market saturation levels at the national-, state-, and county-levels for the following health services: