Valuing ACOs: Weighing the Probability of Shared Savings

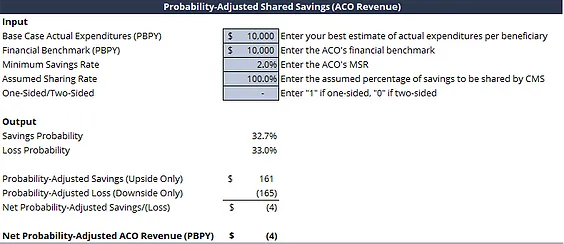

2) If we add an MSR of 2% to the same scenario, the upside, again, is almost identical to the downside, although both are lower due to some probability of the savings rate falling within the risk corridor where none of the savings/loss is shared.

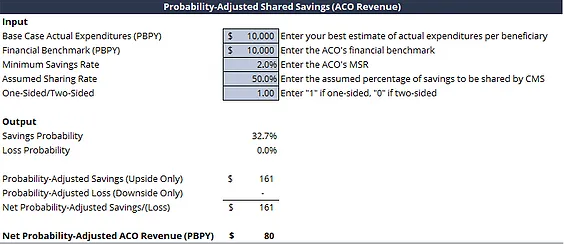

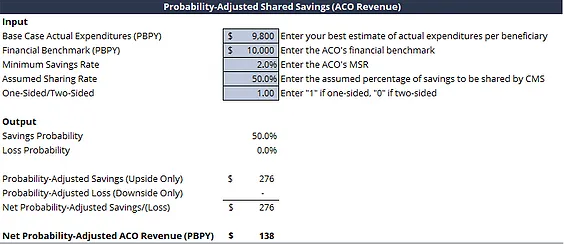

3) Next, if we switch to a one-sided Track 1 MSSP model with a 50% sharing rate, the results look much better ($80), because the possibility of downside loss is eliminated. Note that this figure is fairly similar to the average annual shared savings per beneficiary across the entire MSSP, which has been in the $80-90 range historically.

4) Where it gets interesting is if you change the base case estimate of actual expenditures for the ACO's attributed population. If your ACO is confident it can reduce expenditures by 2.0% against the benchmark ($9,800) as a base case scenario (still subject to a normal level of annual fluctuation), the probability-adjusted shared savings look quite a bit better, for obvious reasons.

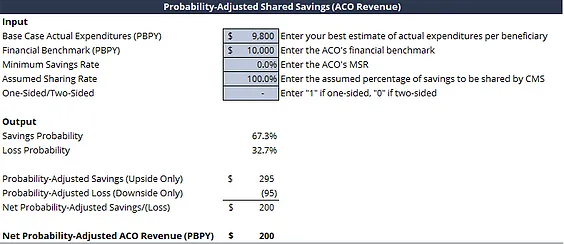

5) However, the optimal option at that point, from a purely-quantitative risk-agnostic standpoint, is to convert to the NextGen model described in scenario 1 where you assume two-sided risk, eliminate the MSR, and receive 100% of the savings or loss. In this scenario, there's still a significant chance of realizing a loss in any given year (32.7%), but the probability-adjusted upside ($295) far outweighs the downside risk (-$95), and the net probability-adjusted ACO revenue is quite a bit higher than in the Track 1 model (scenario 4).

Utility

While the calculator was developed to value ACOs, which we’ve done for a variety of purposes such as mergers and acquisitions, joint ventures, minority investor buy-in/buy-out, and even tax purposes, we think it also may have some utility for ACO executives deciding which of the various financial models to select.

We’re happy to share the model with anyone, just email me at whamilton@buckheadfmv.com and I’ll send you a copy. We also welcome any questions or feedback.

CON Laws, Scope of Practice Restrictions, and Provider Non-Compete Clauses Targeted in New Trump Adm